When creating our new talent experience platform, we aimed to align the fundamental concepts of Cornerstone TXP with our overall vision and belief statements:

- We believe we can empower people to be extraordinary

- We believe business is the greatest platform for change

- We believe nothing changes until someone learns something new

- We believe learning is the force behind innovation, transformation and connection

These are powerful statements by design to evoke inspiration and commitment to our work as talent management and development professionals. For many in this space, we got here because we started our careers with a calling to educate and help others to achieve things beyond what they thought they could.

These beliefs are critical to helping us define our north star with talent management.

Does your organization believe that every employee has the right to access learning and development resources? Or does your organization believe that learning and development resources should be limited to high-potential employees? Consider these types of questions to help set up your own belief statements.

Establishing your why

- Why is this investment, project or change necessary?

- Why is it important to do now?

- What happens if we delay doing it?

There are several ways you can collect data to craft your belief statements:

- Surveys

- Focus groups

- One-on-one meetings

- Anecdotal feedback

When you gather feedback and ideas, it’s important to include diverse representation across your organization. Focus on identifying people from various functions, levels, roles, etc.

According to Gartner’s 2023 CHRO survey and report, open-source change management, whereby changes are co-created with employees, will be 14 times more likely to be successful than those with a top-down-driven approach.

Your belief statements are undoubtedly all about your employees and leaders. Who better to help you create them?

Building your business case

Start with the business! Well, no, duh, the blog’s title is a business case.

What are the goals, objectives, strategies, etc., your organization will be focused on over the next few months, year or years? What is happening in your industry at a macro level? What are your competitors doing? If you were the organization’s CFO, COO, CEO and CHRO, what challenges would you be most concerned about solving and tackling?

You might work for an organization that doesn’t communicate objectives transparently. If that’s the case, talk to as many people as possible to understand the environment — your leader is a great starting point. If your organization publishes financial results, these reports contain a plethora of information about the focus of your business and industry. Another exercise that can be helpful is to conduct a SWOT analysis regarding your business and industry.

The power of three

At Cornerstone, we have a process to help you define your business priories. Internally, we refer to this as the power of three. When we work with our customers, we visually lay out their business priorities in three major themes. The rule of three is a principle in writing that suggests the audience is more likely to remember events or characters if they’re limited to no more than three.

Below is an example of an organization we worked with to identify three critical business priorities, people priorities and, ultimately, the why. We recommend that once you have identified the top three business priorities, you spend some time socializing these and getting confirmation and input from various leaders in your organization.

Aligning your business priorities to your people priorities

The next step in this process is to link your talent priorities to the business's priorities or strategic planning. This helps busy HR and talent teams step back and ensure things align with where the business is headed.

In this example, the organization is growing both organically and through acquisition. One of the top people priorities will be a robust training and onboarding program. If you think about the number of new people entering the organization either by acquisition or as a net new hire, getting them up to speed on the culture, the role, the expectations of their job, etc., will be essential to driving high performance and revenue growth. We know that the faster people can become productive, the more they feel included and the higher their performance output will be.

Defining financial impact

This part of the process is more of an art than a science. Talent initiatives involve multiple variables and one major unpredictable characteristic —humans. However, that does not mean we should throw the towel in and not attempt to quantify and track people’s metrics. Thus, the final step in the process is to define what value impacts you can have based on the business and people’s priorities.

Cornerstone has helped hundreds of organizations and customers over the past two decades to define metrics and business impact. We also work with them to track the metrics and realize value.

We believe that talent management is tied to four key financial metrics.

1. People metrics

- Retention rates

- Engagement scores (ENPS)

- % of roles filled internally

- Leadership pipeline

2. Productivity metrics

- Efficiencies gained

- Improve time-to-productivity (onboarding, change management curve, upskilling, reskilling, etc.)

3. Profitability metrics

- Revenue growth

- Market share

- Wallet share

- Customer retention (NPS)

4. Organizational culture metrics

- Change adoption curve (like onboarding)

- Innovation – speed to market

Example of a financial calculation:

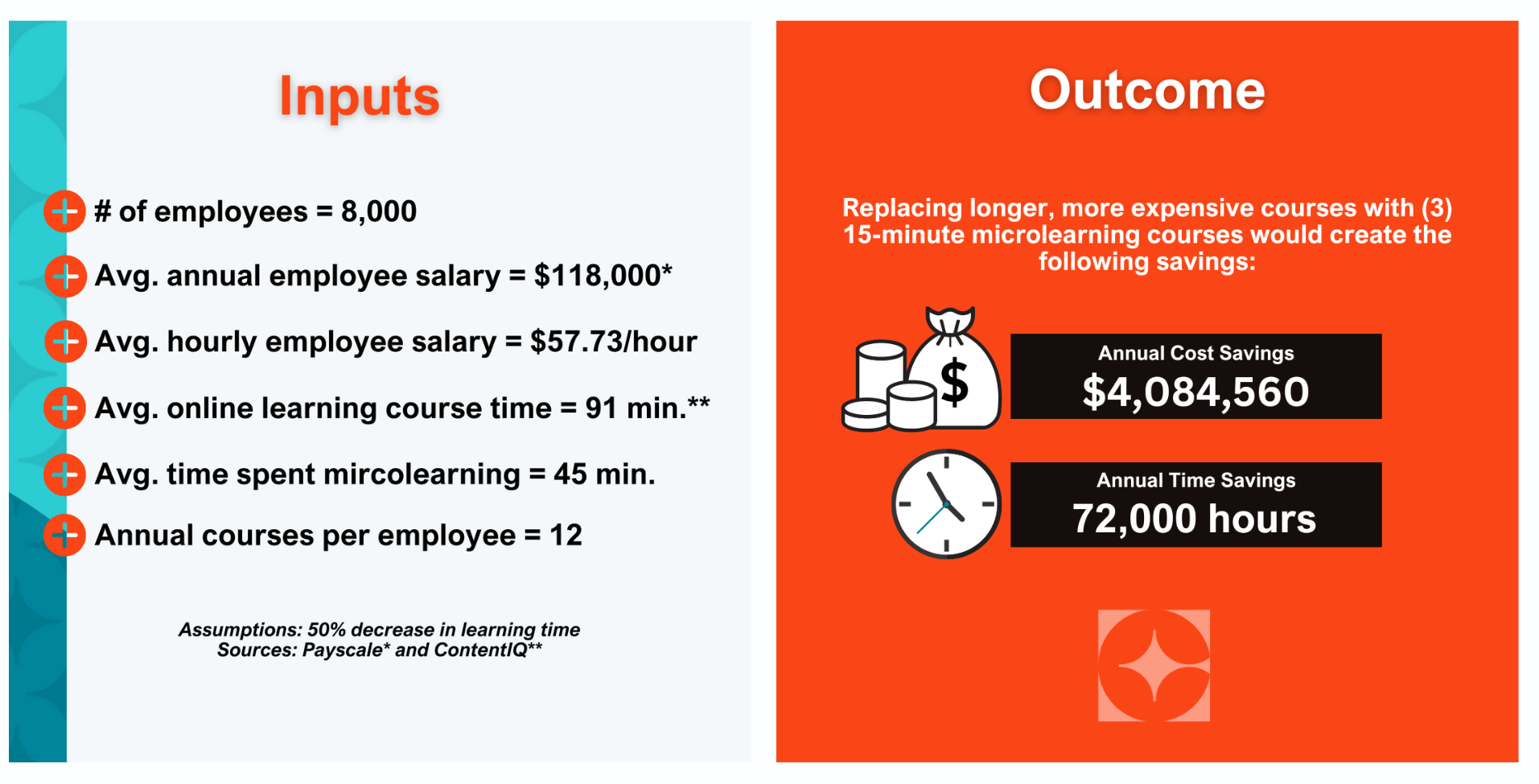

Scenario 1: Content learning efficiency – shifting to microlearning

Customize this calculation for your organization. Using this formula, you can plug in your data and assumptions:

- Number of employees

- Your payroll data – average annual employee salary

- Average length of your existing content

- Average number of courses your employees take annually

- Assumption: this should be a straightforward calculation. If the average course length is two hours and you are switching to microlearning, you can do the math to figure out the decreased learning time

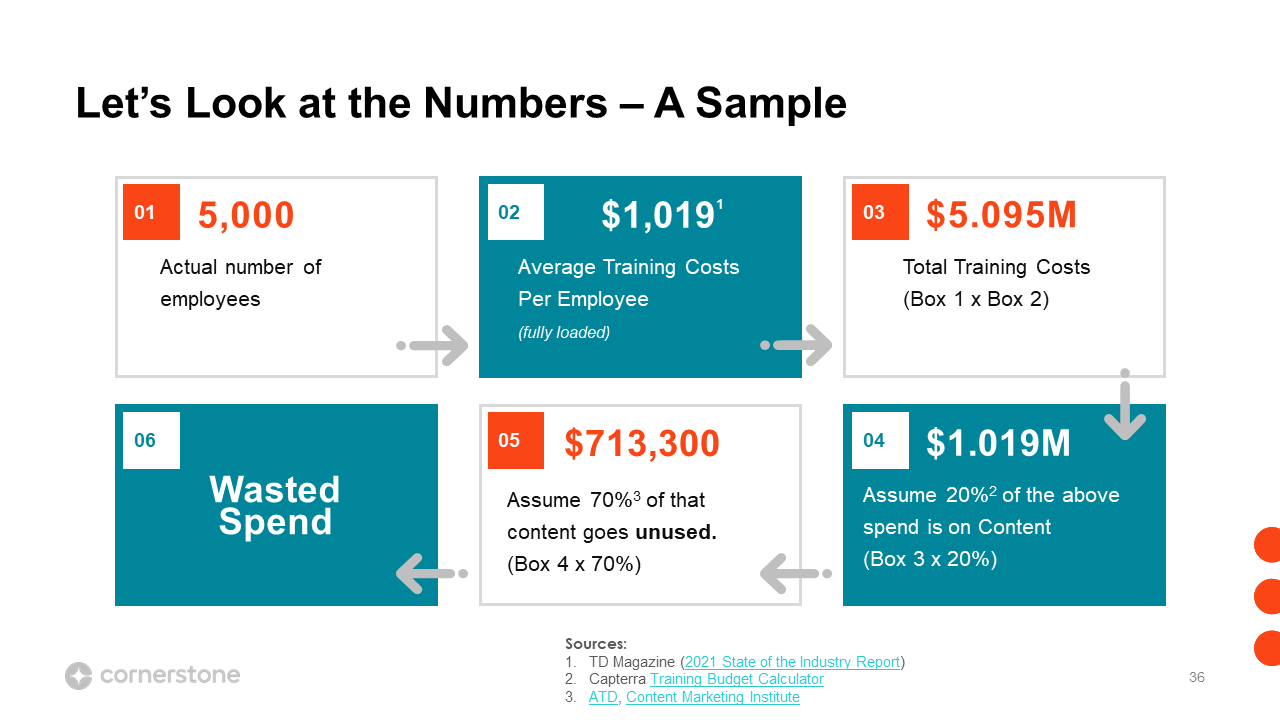

Scenario 2: How much of your content goes unused?

According to ATD, almost 70% of content goes unused. How much money could you save by having targeted content that improves use? Below is an example of how to calculate that waste for your organization.

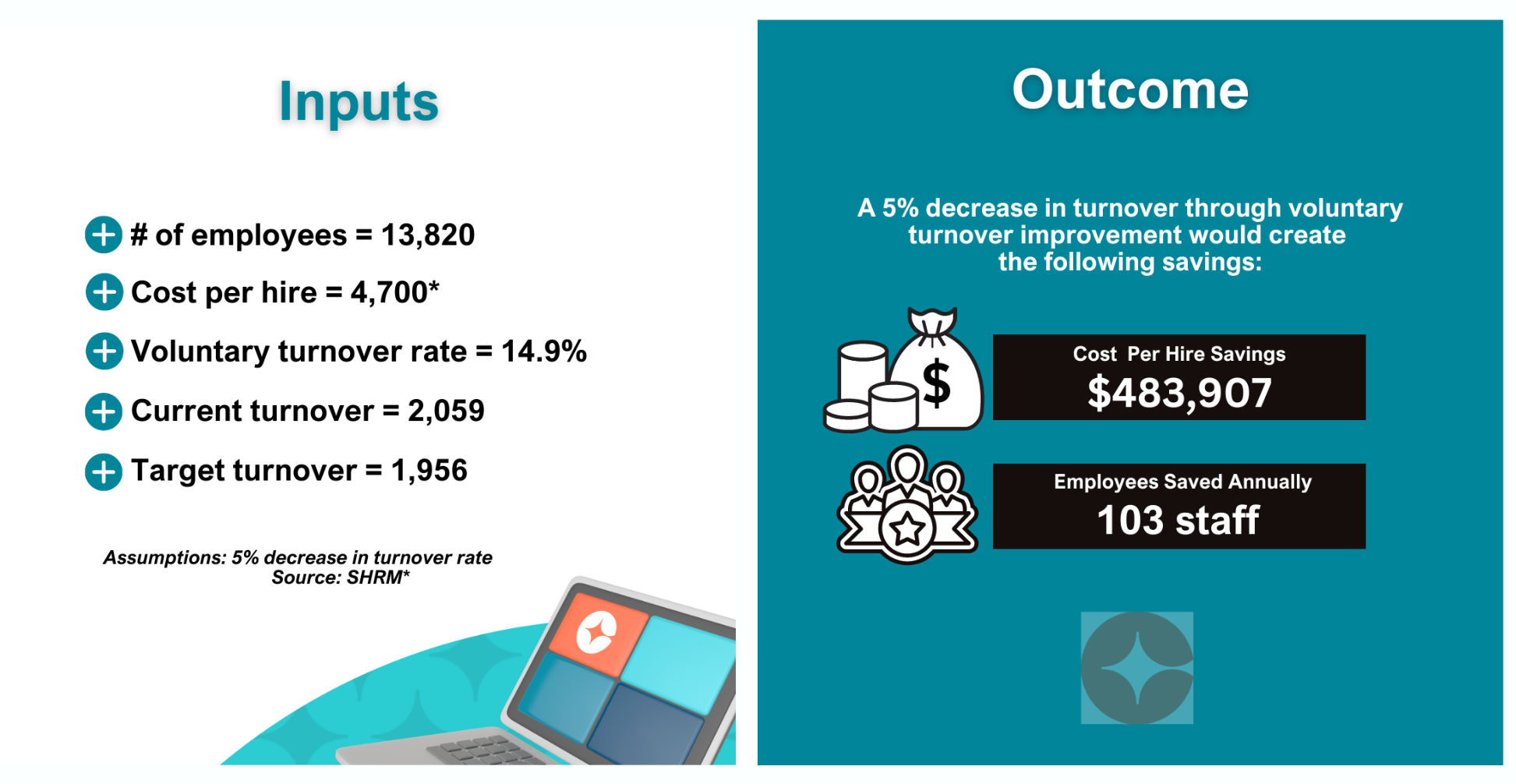

Scenario 3: Reduction in turnover

Employee retention is the easiest and most common metric you can impact across any talent management initiative.

Our retention formula:

- Number of employees X cost of hire X% of turnover

We use a combination of benchmark and research data and our client’s data. The more the data is specific to you, the more impactful it will be.

The cost of hire is the most important factor in this formula. We use SHRM as a benchmark, which is just direct costs — they do not account for indirect costs such as interviewer time, onboarding, etc. In summary, to build your story and business case:

- Define your why

- Identify your business priorities

- Align your people priorities to your business priorities

- Quantify your business impact

By focusing on the “why’s” you establish a link between your organization’s talent and the business’s strategic vision. Hand in hand, this partnership leads to the success of the business.

Start building your talent management business case today. Email cpaxtonhughes@csod.com to speak to a member of our Thought Leadership & Advisory Services team.

To learn how to creatively conquer the business challenges of tomorrow and ensure your people feel passionate about work, download this eBook

co-authored by Dr. Edie Goldberg, an expert in the future of work and talent management.